Condonation in Form, Not in Substance: The Gap in CCFS-2026

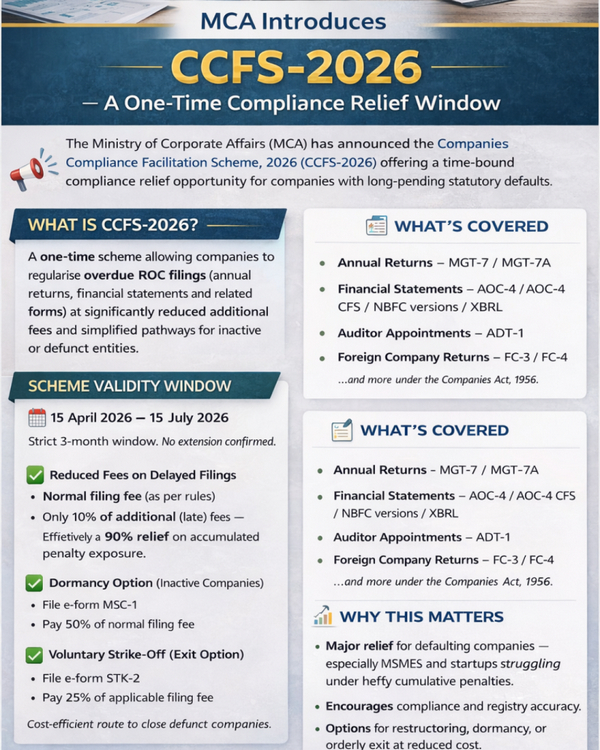

The Companies Compliance Facilitation Scheme, 2026 (CCFS-2026) provides an opportunity for companies to regularize certain long-pending statutory filings. The scheme is proposed to operate for a three month window from 15th April, 2026 to 15th July, 2026, during which eligible companies may complete specified filings by paying the normal filing fee together with only 10% of the applicable additional fees, thereby offering substantial relief from the cumulative additional fee that would otherwise arise on delayed filings.

The scheme primarily covers delayed filings relating to annual compliance documents, including annual returns (MGT-7/MGT-7A) and financial statements (AOC-4 and its variants such as AOC-4 CFS, NBFC versions and XBRL filings). It also allows the filing of certain related forms, such as ADT-1 for appointment of statutory auditor, along with certain filings applicable to foreign companies.

In addition to facilitating delayed filings, the scheme also contemplates structural options for inactive entities. Companies that have temporarily ceased operations may choose to apply for dormant status by filing Form MSC-1 at 50% of the normal filing fee, or alternatively proceed with voluntary strike-off through Form STK-2 at 25% of the applicable filing fee, thereby providing a relatively lower-cost pathway to retain the corporate identity in dormant form or to exit the register.

CCFS-2026 is essentially a filing-centric amnesty and not a cure for all underlying governance violations.

Understanding the Issue Through Two Scenarios

Scenario 1

A company is unable to get its accounts audited within the prescribed time and, consequently, fails to conduct its Annual General Meeting (AGM). As a result, it is also unable to file its annual financial statements and annual returns. This may arise due to closure of operations, oversight on the part of the directors/promoters, or financial constraints preventing the company from completing these compliances.

Scenario 2

A company has been able to get its accounts audited and conduct its AGM within the due date; however, it has failed to file its financial statements or annual returns within the prescribed timeline.

The Structural Gap in CCFS-2026

From a practical perspective, companies in the second scenario are likely to be numerically smaller, since most long-defaulting companies have not even completed audit/AGM for the backlog years. Yet, the structure of CCFS-2026 is drafted around the assumption that filings alone are pending, rather than recognizing that core corporate processes themselves may have remained undone.

This results in a structural gap: companies that defaulted primarily due to their inability to complete audit and conduct AGM within time continue to remain exposed to penal consequences for those substantive lapses, even if they are now willing to regularize their position.

Scope Limitations of the Scheme

Like the earlier “Condonation of Delay Scheme, 2018,” CCFS-2026 focuses narrowly on annual filing compliances, restricted to financial statements and annual returns. It does not extend to other related statutory filings such as Return of Deposits (DPT-3), half-yearly MSME-1, MGT-14 (in case of public companies for approval of accounts), or DIR-3 KYC.